Following on from the report conducted by S&P Global, and which we published on the previous edition (click to access here), we continue with the second part of the main ESG trends that the research firm expects to be in the spotlight of the debate by 2022.

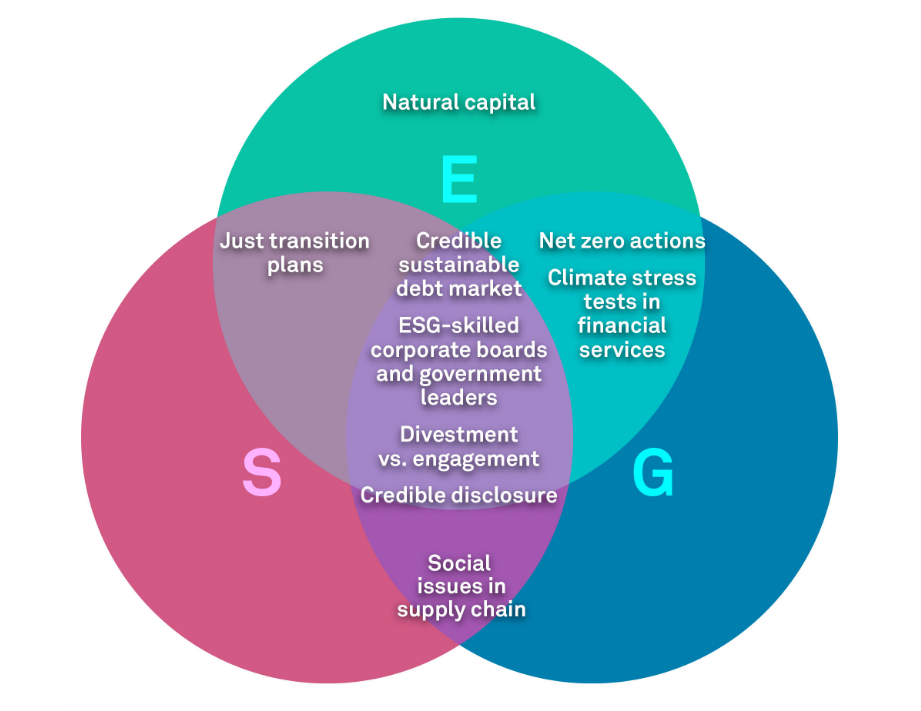

Natural Capital and Biodiversity Gaining Importance

Governments and companies are beginning to advance their commitments to protecting biodiversity and nature in their direct operations. For companies, assessing and managing the supply chains from which materials and inputs are sourced is even more challenging.

Data availability and quality, as well as generally agreed measurement methodologies, remain key challenges. In addition, most of the business world remains uncommitted to stopping deforestation, despite it being easier to measure than other natural capital risks, mainly due to poor understanding of how to assess the benefits of preservation.

On the other hand, the benefits of nature-based solutions, such as wetland, forest and coastal conservation, will continue to gain traction as effective strategies to help adapt to the physical impacts of climate change.

Several major new initiatives in 2022 should contribute to efforts to prioritize biodiversity:

- In late April and early May, the next UN Biodiversity Conference will be held in Kunming, China, where governments will seek to agree on a set of new targets for the next decade under the Convention on Biological Diversity, given that the previous targets set for 2020 were not met. The final text of the new framework will be an important milestone for setting priorities.

- The newly created Task Force on Nature-Related Financial Disclosures will propose a framework for nature-related disclosures, including standards and metrics, as well as data requirements, that will highlight biodiversity and nature commitments.

More Attention to Social Issues in Supply Chains

In 2021, companies were acutely aware of their dependence on supply chains and their fragility. In 2022, S&P Global believes this trend will persist as the global economy continues to recover from the pandemic, and management teams focus on rising supply chain costs and the risk of disruption.

Beyond supply chain resilience, the firm estimates that social issues in supply chains will receive increased attention as efforts to curb human rights abuses and improve labor conditions increase.

Existing and proposed legislation will make supply chain traceability and social risk management more important this year:

- Despite delays to the EU directive on sustainable corporate governance in 2021, mandatory legislation on human rights due diligence at the national level in member states such as Germany, the Netherlands and France will result in a wider swath of companies identifying and acting against human rights violations in their supply chains.

- In addition, continued measures in the United States and other key markets to restrict imports based on forced labor in supply chains will push companies to demonstrate credible human rights monitoring efforts in the chain. This will be the case beyond first-tier suppliers and will include raw materials.

The Divestment vs. Engagement Debate will Heat Up

In 2021, S&P Global notes that more asset owners, managers and banks adopted negative screening strategies, i.e. excluding or divesting from companies with poor ESG practices or high risk exposure.

Such an approach was mostly applied to fossil fuel and other carbon-intensive companies, as well as entities with high acute and chronic physical climate risk. By 2022, the firm expects negative screening to become more widespread, especially for decarbonizing investment portfolios and loan books, increasing the importance of ESG for credit.

Supporters of engagement policies point out that breaking ties with companies through divestment or exclusion does not encourage change, and could result in the sale of such securities to investors less attentive to ESG issues, preferring to use their investments to influence change on key ESG issues, such as climate transition or labor conditions in the supply chain.

Testing the integrity of the sustainable debt market

In 2021, total sustainable debt issuance reached a record high of about $960 billion, according to preliminary estimates from the Environmental Finance Bond Database. This figure includes green, social and sustainability-linked bonds and represents a 61% increase in just one year.

Based on historical trends, there is room for continued growth, if not acceleration in 2022, as companies and governments seek to finance the transition to a net zero economy.

A key challenge for market participants in the coming year will be to manage this growth in a way that preserves the legitimacy of these financing instruments and combats growing concerns about greenwashing.

Indeed, S&P Global indicates that diversification and innovation in sustainable debt instruments is likely to continue, with the risk of further fragmentation across issuers, instruments, sectors and standards.

For example, for sustainability-linked instruments, which are poised for strong growth in 2022, market participants should be vigilant to ensure that issuers set appropriately ambitious performance targets and maintain transparency throughout the life of the instrument through regular, high-quality disclosure.

Therefore, efforts to establish and encourage the adoption of clear standards and frameworks will be critical in 2022 to protect the integrity of the sustainable debt market as it reaches new heights.