The growing urgency toward energy neutrality and transition is encouraging companies to innovate even more in the pursuit of premium sustainable petrochemicals, which in turn, is driving rapid growth in demand for the feedstocks to produce them and resulting in an increasingly tight market.

According to the Breaking Barriers to Accelerate Energy Transition report by S&P Global, the main innovations are chemical plastics recycling and bioplastics, which refer to both plastics made from bio-based feedstocks and end-of-life biodegradable plastics.

More than 7.8 million metric tons per year (mt/year) of capacity was certified for biopolymer production worldwide by the end of 2021, according to data from the International Sustainability and Carbon Certification (ISCC), and more than 1.4 million mt/year of chemical recycling capacity is expected to come online by 2025, according to research from S&P Global Commodity Insights.

However, this is a figure that looks small in the face of the overall size of the plastics market: production is estimated at more than 300 million mt/year.

According to the Ellen MacArthur Foundation, a UK-based promoter of the circular economy, companies accounting for 20% of all plastic packaging produced worldwide have committed to using recycled and recyclable plastic and reducing their reliance on virgin (fossil fuel-derived) plastics.

Key barriers

Inadequate availability of raw materials is a major obstacle, whether it is the supply of post-consumer plastic waste, for mechanical or chemical recycling, or the supply of first, second or third generation feedstocks for biopolymer production.

In the case of recycled plastics, it means navigating complex waste collection systems that are not uniform even within a single country, as well as in the case of bioplastics, where petrochemical companies will have to compete for binafta, the main feedstock, with gasoline blending markets and agriculture.

Solving feedstock supply issues will be key to driving scalability, increased competition and technological innovation throughout the supply chain.

Another issue is recycling. One example is that recycling capacity in the U.S. would have to increase by at least 50% over current levels to meet announced commitments by companies operating in the U.S., according to a 2021 study by the American Institute for Packaging and the Environment.

According to S&P Global, this problem is not specific to the U.S.: Global recycled plastic prices followed a strong upward trend throughout 2021 as a result of growing demand, acute supply shortages and shipping disruptions that have cut off vital sources of supply, such as Southeast Asia from European and U.S. demand centers.

Bioplastics

The key petrochemical feedstock for the production of bioplastics is bionaphtha, which can be used as a direct substitute for fossil-based naphtha.

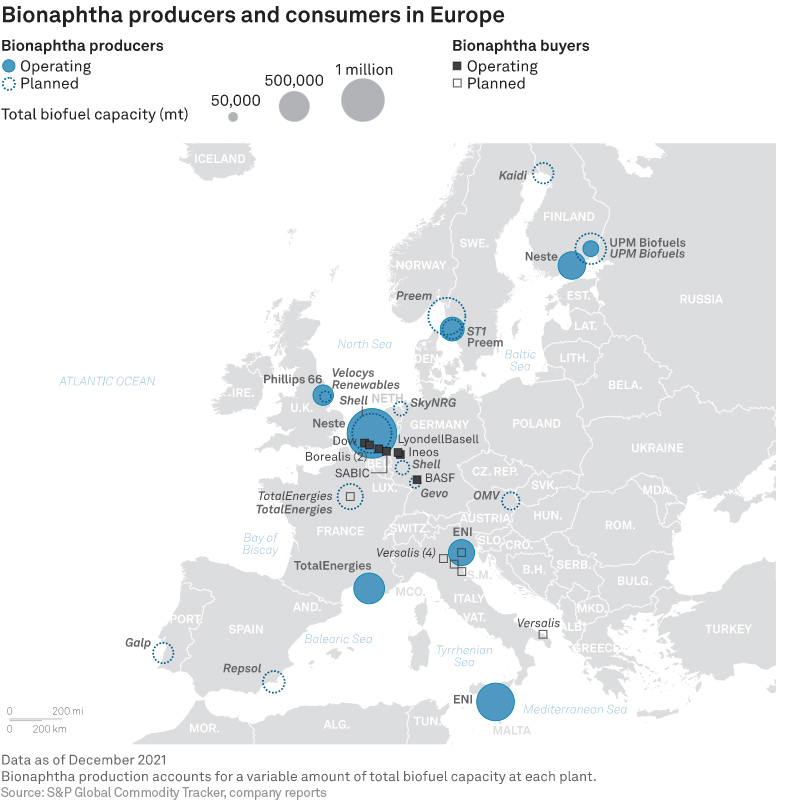

The current supply of binafta in Europe is estimated at between 150,000 and 250,000 tons per year, with expectations of doubling or even exceeding 1 million tons per year in the coming years, according to the NOVA Institute. Even in the most optimistic scenario, bionaphtha supply would not meet demand growth expectations.

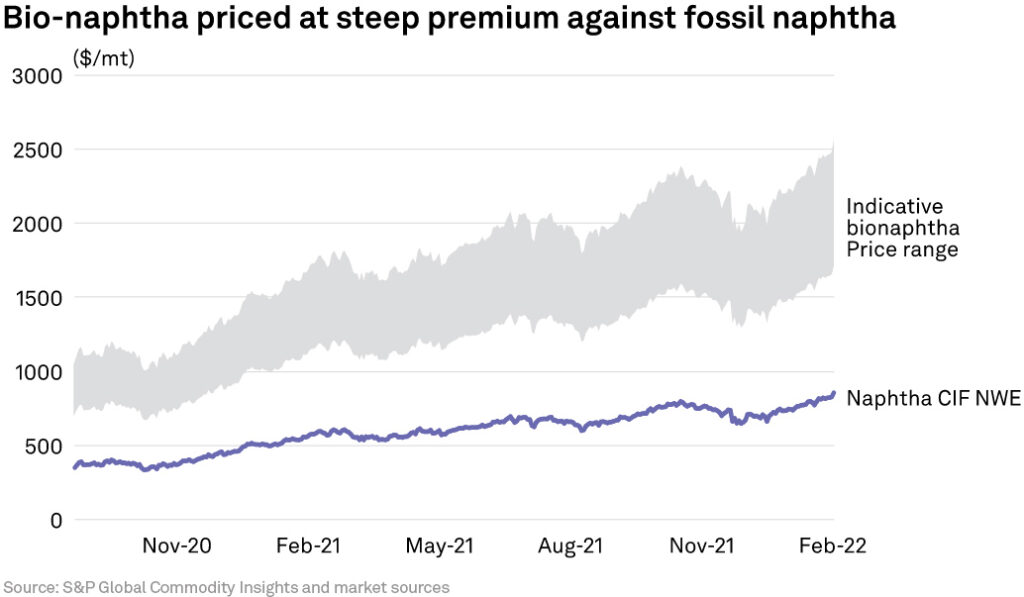

As a result, bionaphtha is typically priced well above its fossil alternatives, which can be double to triple the price of Platts CIF NWE benchmark naphtha.

For S&P Global, petrochemical markets are going to have to attract this key sustainable feedstock in the face of strong competition, from the food and fuels industry, if sufficient quantities of biopolymers are to be scaled up and supplied.

Reducing emissions

Several petrochemical producers are stepping up their carbon reduction efforts in sectors such as methanol, olefins and polymers, including PET (polyethylene terephthalate). Solutions include the use of renewable energy, increased bioproduction, carbon capture, utilization and storage technology, and switching from fossil fuel-based feedstocks to lower-carbon alternatives such as hydrogen.

On the other hand, the S&P Global report points out that the results obtained so far are far from the target. Among the solutions are:

- More coherent policy frameworks will be needed, particularly in emerging petrochemical hubs, to reduce barriers to investment in these new technologies.

- It will require industry efforts to standardize how the carbon intensity of particular petrochemical products is measured and reduced, or offset in carbon credit markets.

- Greater standardization and liquidity would drive competition and technological innovation, and facilitate the formation of prices and benchmarks that would ultimately determine the direction and pace of change through the energy transition.

For the financial research firm, there are multiple routes to a greener future for petrochemicals and they will need to be explored simultaneously for the industry to be truly green.

“To get to the stage where a plastic bottle, for example, is made of part recycled content, part bio-based content and part certified low-carbon material, all of these markets will require efforts to drive commoditization on a global scale,” the report states.

To access the S&P Global research report, click here